As medical marijuana gains traction as a legitimate treatment option, many patients wonder whether their health insurance will cover its cost. While the legal landscape continues to evolve, the answer for now is mostly no. Medical marijuana’s classification as a controlled substance under federal law complicates insurance coverage, and most policies, including Medicare and Medicaid, do not cover it. However, there are nuances to consider as the situation changes.

The Federal Legal Status of Cannabis

The key barrier to insurance coverage is marijuana’s classification as a Schedule I drug under the Controlled Substances Act. This designation means that cannabis is considered to have a high potential for abuse and no accepted medical use at the federal level. Despite medical marijuana being legal in 38 states, this federal status ties the hands of insurers. However, there is increasing momentum to reclassify cannabis as a Schedule III drug, which would recognize its medical potential but still require FDA approval for specific products to be covered by insurance.

FDA-Approved Cannabis-Based Medications

While most cannabis products remain illegal at the federal level, the FDA has approved a few cannabinoid-based medications that may be covered by insurance. These include:

- Marinol and Syndros (synthetic THC) for nausea and appetite loss in chemotherapy and HIV patients.

- Cesamet for chemotherapy-related nausea.

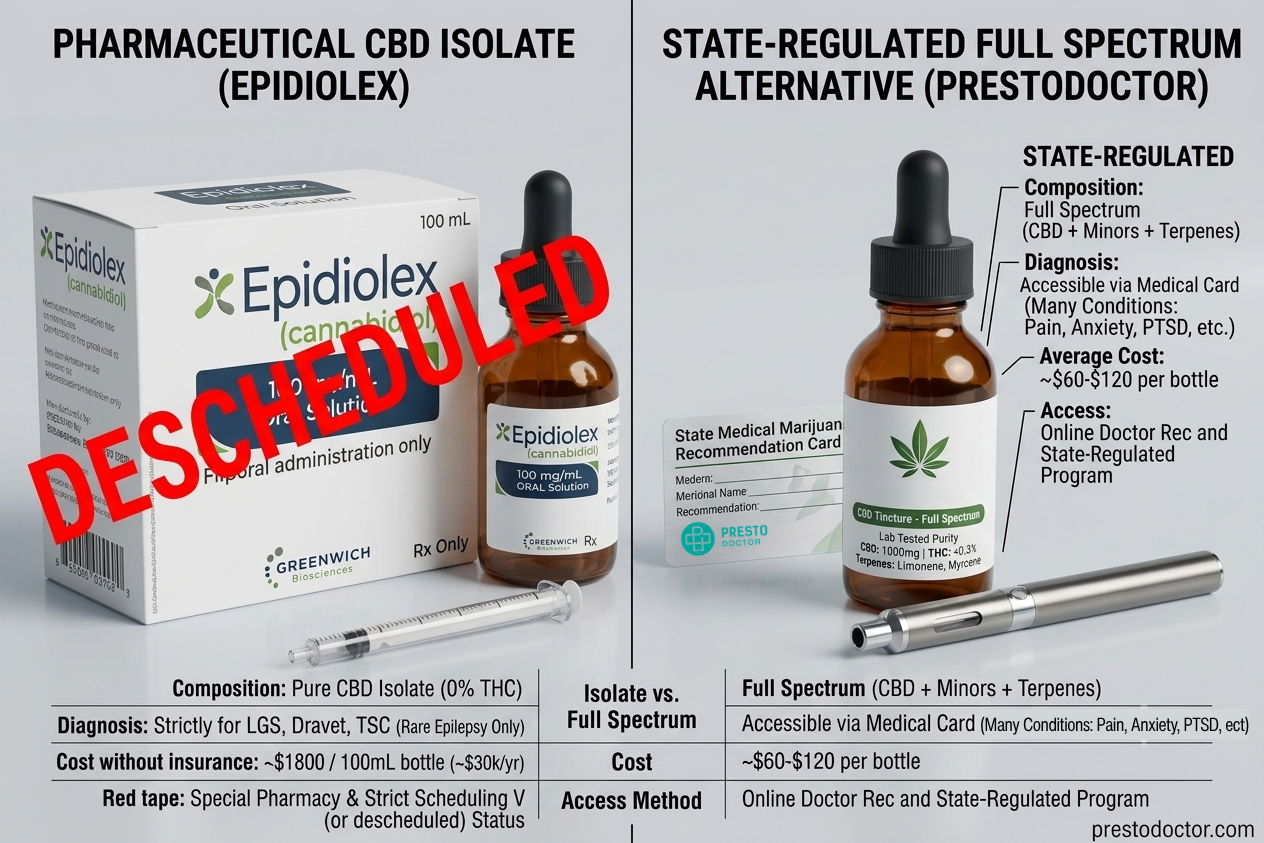

- Epidiolex, a cannabidiol (CBD) treatment for epilepsy.

These FDA-approved medications can appear on insurance drug formularies, meaning some level of coverage is possible for these specific treatments.

Medicare’s Stance on Medical Marijuana

Medicare, which serves individuals over 65 and those with disabilities, does not cover medical marijuana because it is federally illegal. However, Medicare Part D may cover the FDA-approved medications mentioned earlier, such as Epidiolex and synthetic THC products like Marinol and Syndros. This limited coverage is available because these drugs have passed through the FDA approval process.

Medicaid’s Position on Medical Marijuana

Medicaid, the health program for low-income individuals, also does not cover medical marijuana due to federal regulations. Since Medicaid is funded by both federal and state governments, it cannot cover treatments that are illegal under federal law. However, Medicaid does cover the FDA-approved cannabinoid drugs like Epidiolex, which may offer some relief for patients in need.

Private Insurance and Medical Marijuana

While private insurance largely mirrors federal policy, there are some exceptions. In states like New York and New Jersey, legislators are pushing for insurers to cover medical cannabis under certain conditions. However, these initiatives have yet to become widespread. Until cannabis is legalized federally or gains more FDA approvals, most private insurers will not cover medical marijuana.

Workers’ Compensation and Medical Marijuana Coverage

In some states, courts have ruled that workers’ compensation insurers must cover medical marijuana for injured workers. States like New Hampshire and New Mexico have seen court rulings in favor of reimbursement, while states like Maine and Minnesota have ruled against it due to federal law. If cannabis is reclassified to Schedule III, this could open the door to more favorable rulings for patients seeking compensation coverage.

Future of Coverage: Cannabis Reclassification

The reclassification of cannabis from Schedule I to Schedule III would signal a shift in how insurance companies might approach medical marijuana. While this would make cannabis more acceptable for medical use at the federal level, it does not automatically mean that insurance companies will cover it. Products would still need FDA approval to be included in insurance drug formularies.

CBD Coverage and Alternative Options

CBD, a non-psychoactive component of cannabis, is another area of interest. Epidiolex, the only FDA-approved CBD medication, is covered by some insurance plans, but non-prescription CBD products are typically not covered. Patients looking for cost-effective alternatives to insurance coverage may consider obtaining a medical marijuana card, which can provide access to discounts and tax benefits in states where it is legal.

Affordable Alternatives for Patients

Since insurance won’t cover medical marijuana, patients can explore alternative options to reduce costs:

- Medical marijuana cards for discounts or tax exemptions.

- State hardship programs for low-income patients.

- Home or caregiver cultivation in states where it’s allowed, providing a cheaper option for accessing cannabis.

Conclusion

For now, insurance coverage for medical marijuana remains limited, but there are signs that this could change in the future. As the legal and regulatory environment continues to shift, patients should stay informed about potential changes in federal law, FDA approvals, and state-specific programs that could open doors to broader coverage. Until then, understanding the current landscape can help patients explore alternative ways to manage their medical cannabis costs.